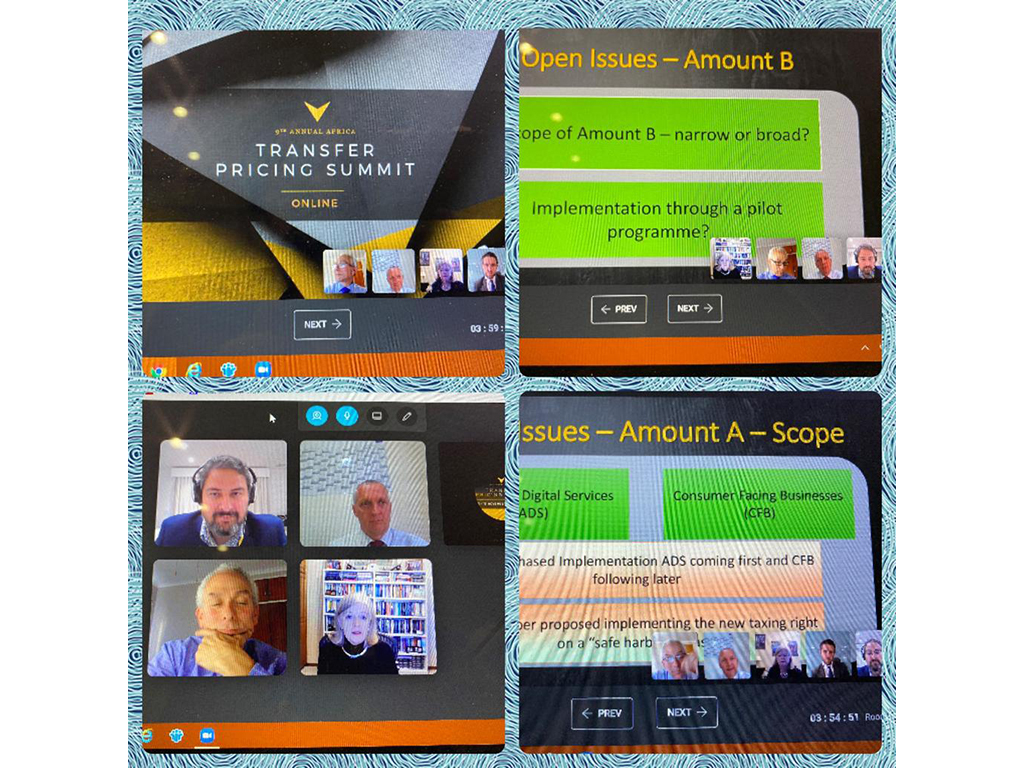

TPED responds to a call for comments by the OECD

December 2020

TPED has provided comments on the OECD Public Consultation Documentation named “Reports on the Pillar One and Pillar Two Blueprints published on 12 October 2020”.

TPED has provided comments on the OECD Public Consultation Documentation named “Reports on the Pillar One and Pillar Two Blueprints published on 12 October 2020”.

Three members of TPED, Sébastien Gonnet, Romero Tavares, Michael Hewson were invited to speak at the 2020 Transfer Pricing Conference of SAIT (South-African Institute of Taxation).

Ednaldo Silva, founder of RoyaltyStat, also a member of TPED, has recently published an article about safe harbors in retail that can be applied to any industry, provided that the source data reflect the specific industry of interest.

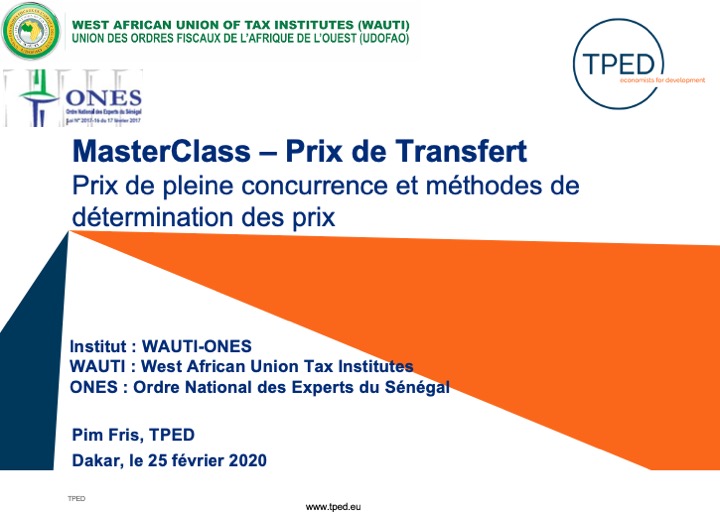

The masterclass has been delivered in the context of the 6th Fiscal Conference of the Union des Ordres Fiscaux de l’Afrique de l’OUEST (UDOFOA/WAUTI).

Transfer Pricing Expert, Oliver Treidler, publishes extensive comments on TPED’s Research Paper on MNE Tax.

TPED invited to speak at IBFD 5th African Tax Symposium – Trends in International Taxation: An African Perspective, in Cape Town, South- Africa.

TPED President Sébastien Gonnet presented on The Elusive Search for Comparables in Africa – a proposed process. Mr Gonnet’s presentation took place in the context of a panel covering Transfer Pricing led by Emily Muyaa.

Ednaldo Silva, Founder of RoyaltyStat, also a member of TPED, published Location Savings Adjustments to Profits in Journal of International Business and Economics (Silva, Location Savings Adjustments to Profits, JIBE, Volume 19 n°1 19 – https://www.royaltystat.com/assets/docs/RoyaltyStatLocSavAdjTP.pdf). It follows the publication of Silva, Pygmalion Comparables: Why Data from the “Center” Does Not Apply for “Periphery”, BNA Tax 23/2015, 1 (1 et seq) https://issuu.com/ednaldosilva/docs/ednaldo_silva_-_pygmalion_comparabl.

TPED partners with taxsutra.com to launch a research project looking at “Analyzing from a Comparability Perspective, the Mark-ups Observed in India”.

Prof. Matthias Petutschnig, from WU and also a member of TPED, and Stefanie Chroustovsky from WU, publish Comparability Adjustments A Literature Review (WU International Taxation Research Paper Series No. 2018-08, 1 Oct 2018).

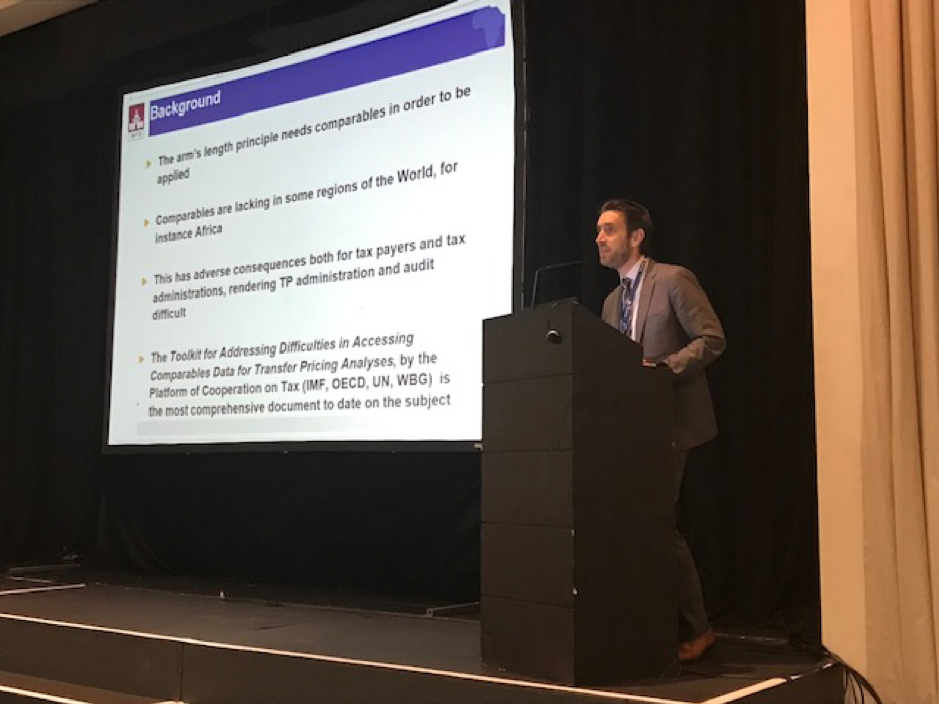

TPED invited to speak at IBFD 4th African Tax Symposium – Trends in International Taxation: An African Perspective, in Mombasa, Kenya. TPED President Sébastien Gonnet presented on The Elusive Search for Comparables in Africa in a panel session covering Transfer Pricing in Africa, chaired by Emily Muyaa. The presentation aimed at evaluating the various options available to tax authorities and tax payers to cope with the lack of comparables in Africa. Aligned with the work done by the Platform of Cooperation on Tax (IMF, OECD, UN, WBG), Mr Gonnet discussed two options to establish local arm’s length ranges / safe harbors: